How Much Down Payment Do You Need for a DSCR Loan?

If you’re looking to finance an investment property using a DSCR loan, one of the first questions you’ll have is: how much down payment do I actually need? The short answer is—more than a typical primary residence loan, but often less restrictive than you might expect. DSCR (Debt Service Coverage Ratio) loans are designed specifically for real estate investors. Instead of focusing on your personal income, lenders look at the property’s ability to generate income. Because of that flexibility, down payment requirements are structured a bit differently than traditional loans. If you’re new to these programs, you can learn more about how they work on our DSCR loan program page.Typical Down Payment for a DSCR Loan

Most DSCR loans require a down payment between 20% and 25% of the purchase price. However, the exact amount can vary depending on the property, your experience as an investor, and the lender you’re working with.- 20% down is common for strong deals with solid rental income

- 25% down is typical for most scenarios

- 30%+ may be required for higher-risk properties or lower DSCR ratios

The 5 Key Factors That Determine Your DSCR Down Payment

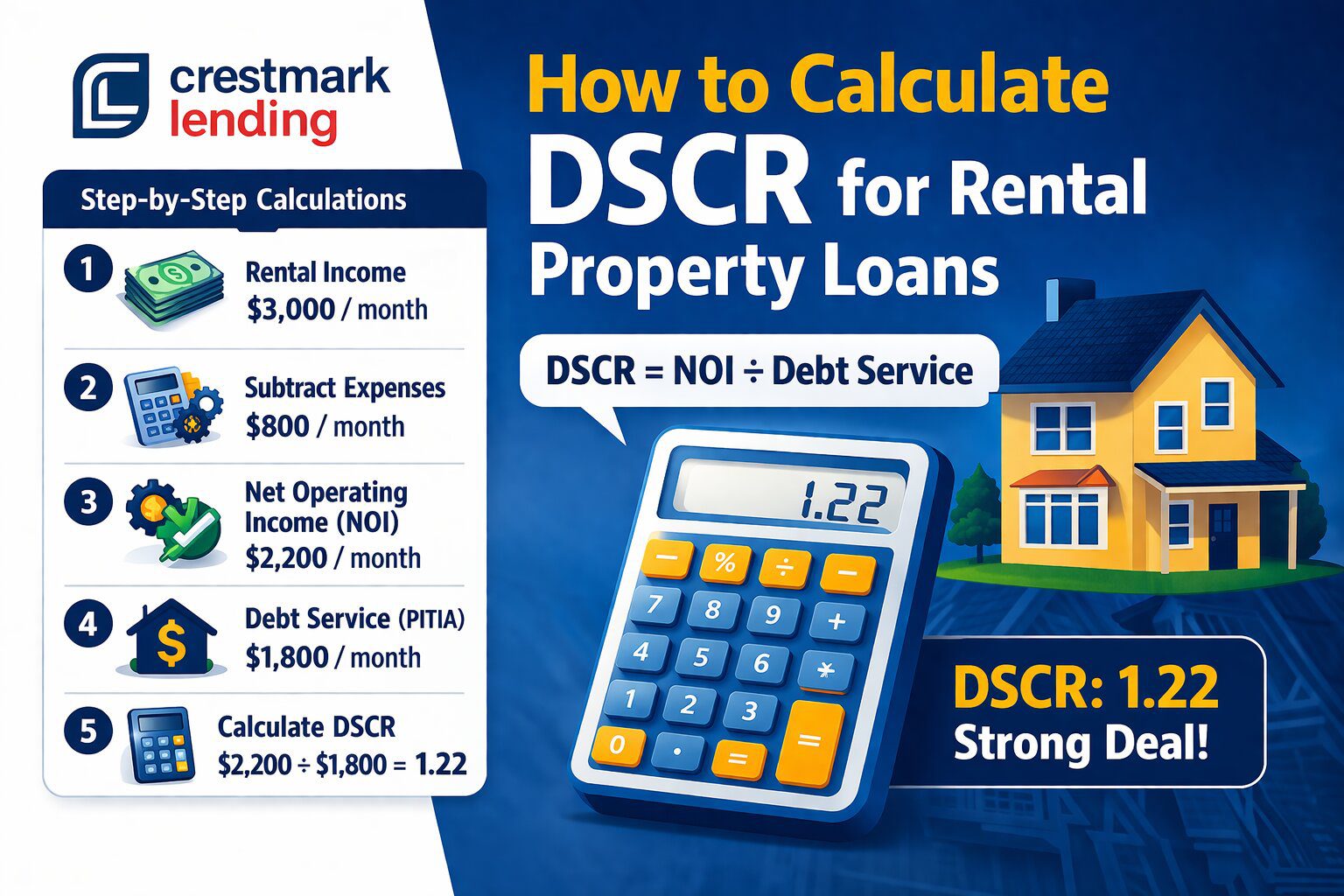

1. DSCR Ratio

Higher cash flow relative to the mortgage payment can improve your terms

2. Property Type

Single-family homes often require less down than short-term rentals or multi-units

3. Credit Score

Better credit can help you qualify for lower down payment options

4. Loan Amount

Larger or smaller deals may come with different requirements

5. Investor Experience

First-time investors may be asked to put more down

Can You Put Less Than 20% Down?

In most cases, DSCR loans require at least 20% down. Unlike primary residence loans, there are no ultra-low down payment options like 3% or 5%. Some lenders may offer slightly lower down payment options in specific situations, but those typically come with higher interest rates or stricter requirements. It’s important to weigh the trade-off between leverage and cash flow.Why DSCR Loans Require Larger Down Payments

Since DSCR loans don’t rely on personal income verification, lenders offset that risk by requiring more equity upfront. A larger down payment:- Reduces the lender’s risk

- Improves your loan terms

- Helps ensure the property cash flows

How the DSCR Loan Process Works

If you’re considering using a DSCR loan, understanding the steps can help you move faster when you find the right deal. From pre-qualification to closing, the process is typically more streamlined than traditional financing. You can see a full breakdown of what to expect on our DSCR loan process page.How to Decide What to Put Down

While 20–25% is standard, the right down payment depends on your investment strategy:- Want stronger cash flow? Consider putting more down to lower your payment

- Want to scale faster? Stay closer to 20% to preserve capital for additional properties

- Buying in a higher-risk market? A larger down payment can provide more cushion

The Bottom Line

Most DSCR loans require a down payment of 20% to 25%, with adjustments based on the strength of the deal and your overall investor profile. While that may be higher than traditional home loans, it comes with more flexible qualification and a focus on property income instead of personal income. If you’re planning your next investment, understanding your down payment options is key. With the right structure, you can build a portfolio that grows while still maintaining strong cash flow.Ryan Collins is the founder of Crestmark Lending, specializing in DSCR loans for real estate investors nationwide. He works closely with investors to structure deals based on property cash flow, navigate lending guidelines, and secure competitive financing—helping clients scale their portfolios with flexible, income-based loan solutions.

Latest blog posts

Request a DSCR Refinance Quote

We’ll review your scenario and contact you with available financing options.

"*" indicates required fields

Request a DSCR Purchase Quote

We’ll review your scenario and contact you with available financing options.

"*" indicates required fields

Get Started – Quick Rate Quote

"*" indicates required fields

Mortgage Rate Assumptions

* Rates shown assume a purchase transaction.

* Annual Percentage Rate (APR) calculations assume a purchase transaction of a single-family, detached, owner-occupied primary residence; a loan-to-value ratio of less than 80% for conventional loans; a minimum FICO score of 740; and a loan amount of $300,000 for conforming loans, unless otherwise specified.

* Annual Percentage Rate (APR) calculations assume a purchase transaction.

* Rates may be higher for loan amounts under $300,000. Please call for details.

* Rates are subject to change without notice.

* Closing Costs assume that borrower will escrow monthly property tax and insurance payments.

* Subject to underwriter approval; not all applicants will be approved.

* Fees and charges apply.

* Payments do not include taxes and insurance.

* Assumes – 30 Day Rate Lock.

* Rates based on Texas property.

* Mortgage insurance is not included in the payment quoted. Mortgage insurance will be required for all FHA, VA and USDA loans as well as conventional loans where the loan to value is greater than 80%.

* Restrictions may apply.

* Lender Fees & Appraisal Fees may apply