How to Calculate DSCR for Rental Property Loans (Step-by-Step Guide)

If you’re investing in real estate, understanding how to calculate DSCR is one of the most important skills you can have. If you are not familiar with DSCR loans, check out our “What is a DSCR Loan” blog.

DSCR loans are built around one simple idea: does the property make enough money to pay for itself?

In this guide, we’ll break down exactly how to calculate DSCR, walk through a real example, and show you how to use the Crestmark Lending calculator to run your numbers quickly.

What Is DSCR?

DSCR stands for Debt Service Coverage Ratio. It’s the number lenders use to determine whether a rental property generates enough income to cover its loan payments.

Instead of focusing on your personal income, DSCR loans qualify you based on the property’s cash flow.

In simple terms:

- If the property makes more than it costs → you’re in good shape

- If it barely breaks even → approval gets tougher

- If it loses money → most lenders will decline

How To Calculate DSCR

Not sure if your deal qualifies? Use this formula—or skip the math and get instant results using our DSCR calculator.

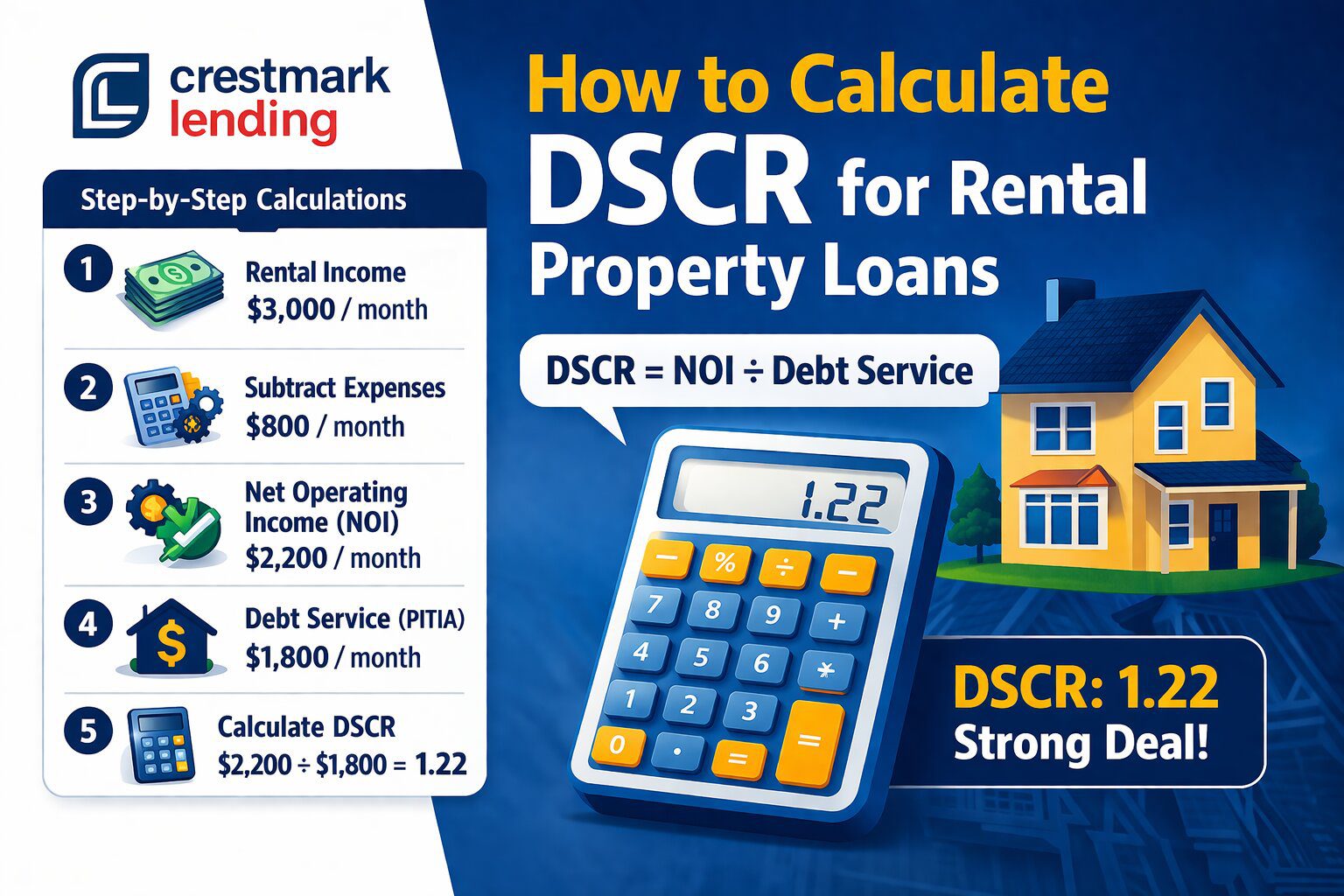

DSCR = Net Operating Income (NOI) ÷ Total Debt Service

Net Operating Income (NOI) = Rental income minus expenses (taxes, insurance, maintenance, etc.) Debt Service = Total monthly mortgage payment (PITIA – principal, insurance, taxes, insurance, association fees)- Rental Income ($3,000/mo.) – Expenses ($800/mo.) = NOI ($2,200/mo.)

- Debt Service = $1,800/mo.

DSCR: 2,200 ÷ 1,800 = 1.22 (Strong Deal)

This means the property generates 22% more income than needed to cover the loan—typically considered a strong DSCR for most lenders.What Is a Good DSCR?

Most lenders look for a DSCR of at least 1.20 to 1.25.

- 1.00 DSCR → Break-even (income = expenses)

- 1.20+ DSCR → Strong deal (preferred by lenders)

- 1.50+ DSCR → Excellent cash flow

The higher your DSCR, the easier it is to qualify—and often the better your loan terms.

How the Crestmark Lending DSCR Calculator Helps

If you don’t want to run these numbers manually every time, you can use the Crestmark Lending DSCR calculator.

It simplifies the entire process by letting you plug in:

- Rental income (To get the most accurate DSCR, start by getting an estimated rental income.)

- Property expenses

- Loan terms

- Estimated monthly payment

From there, it instantly calculates your DSCR and helps you understand whether your deal meets lender guidelines.

This is especially helpful when you’re analyzing multiple properties or comparing investment scenarios side by side.

Common Mistakes When Calculating DSCR

Even experienced investors can get this wrong. Here are the most common issues:

- Using gross rent instead of NOI (forgetting expenses)

- Underestimating repairs and vacancy

- Leaving out taxes or insurance

- Using unrealistic rent projections

Accurate inputs matter—because even small miscalculations can significantly impact your DSCR.

Why DSCR Matters for Investors

DSCR loans are popular because they allow investors to scale without relying on personal income verification.

Instead, lenders focus on what really matters: the performance of the property itself.

This makes DSCR loans ideal if you:

- Own multiple properties

- Are self-employed or have complex income

- Want to grow a rental portfolio faster

Since approval is based on cash flow, strong deals can often qualify even when traditional loans fall short.

Final Thoughts: Keep It Simple

At the end of the day, DSCR is just a quick way to answer one question:

Does this property make financial sense?

If the income comfortably covers the debt, you’re on the right track.

If not, it may be time to renegotiate, raise rents, or look for a better deal.

And if you want to speed up your analysis, the Crestmark Lending calculator is one of the easiest ways to run your numbers and move quickly on opportunities.

This article was written by Ryan Collins of the Crestmark Lending team to help real estate investors understand how to calculate DSCR and evaluate rental property deals with confidence. It provides clear, practical insight into analyzing cash flow, estimating income, and using DSCR to qualify for investment property financing.