What Credit Score Do You Need for a DSCR Loan?

If you’re investing in real estate, you’ve probably heard about DSCR loans—and how they don’t require traditional income documentation. But one of the most common questions we get is simple:What credit score do you actually need to qualify?

Let’s break it down in a way that’s easy to understand so you know exactly where you stand. The Short Answer–Most DSCR lenders require a minimum credit score somewhere in the 620 to 660 range. That said, your experience—and your loan terms—can vary quite a bit depending on your score.How Credit Score Affects Your DSCR Loan

While 620 might technically qualify, there’s a big difference between getting approved and getting a great deal. Here’s how lenders typically view different credit ranges:- 620–659: You may qualify, but expect higher rates, stricter terms, and potentially a larger down payment.

- 660–699: More options open up with better pricing and flexibility.

- 700+: This is where things really improve—better rates, higher leverage, and smoother approvals.

- 740+: Top-tier borrower with access to the best terms available.

Why Credit Still Matters for DSCR Loans

A lot of investors assume DSCR loans don’t look at personal finances at all. While it’s true that your income isn’t used to qualify, your credit score still plays a key role in how lenders evaluate risk. Your score can directly impact:- Interest rate

- Down payment requirements

- Loan-to-value (LTV)

- Cash reserve requirements

- Overall approval strength

What’s the Lowest Credit Score Possible?

Some lenders may go below 620, but there are trade-offs.- Higher down payments (often 25–35%)

- Higher interest rates

- More conservative loan terms

DSCR Loan Eligibility Guidelines

Exact DSCR lender guidelines vary — we shop them for you and select the best match.

Credit Score Requirements

Program Type

Minimum FICO

Best Pricing

Standard DSCR

620–660+

700+

STR / Airbnb DSCR

640–660+

700+

Low DSCR (<1.0)

660+

700+

Multi-Family (2–8 units)

660+

700+

What Else Do You Need Besides Credit?

Your credit score is just one piece of the DSCR loan equation. Most lenders will also look for:- 20–25% down payment

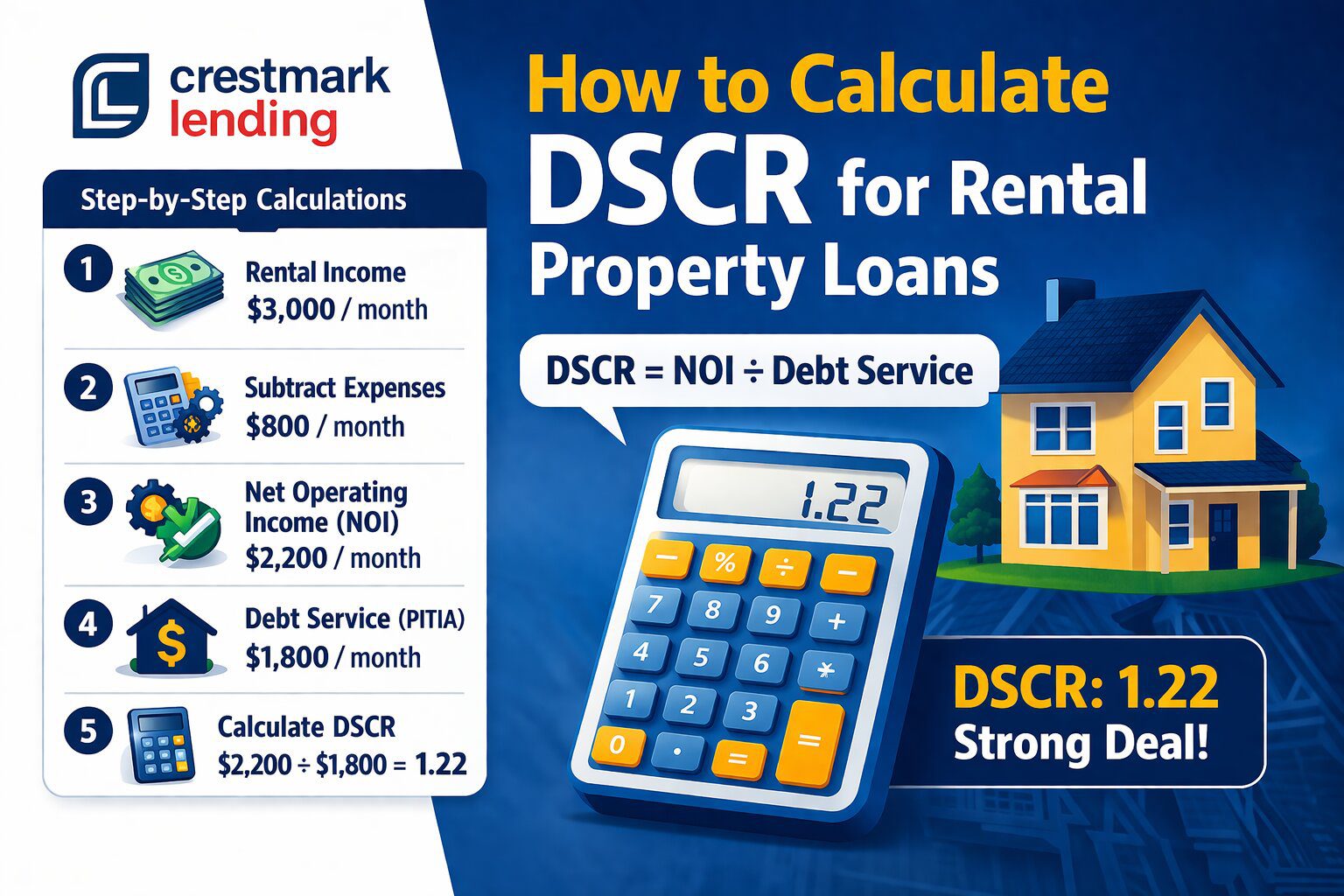

- A DSCR ratio around 1.0–1.25 or higher

- Cash reserves (typically 3–6 months)

Pro Tip: Small Credit Improvements Make a Big Difference

A small bump in your credit score can go a long way. Even a 20–40 point increase can improve your rate, lower your monthly payment, and increase your long-term cash flow. If you’re close to 700, it may be worth taking a little time to improve your score before applying. Not sure where your credit currently stands? You can check your credit for free through trusted sources like AnnualCreditReport.com, which is authorized by the federal government.Final Thoughts

So, what credit score do you need for a DSCR loan?- Minimum: Around 620

- Ideal: 700+

- Best terms: 740+

Ryan Collins is the founder of Crestmark Lending, a DSCR loan specialist serving real estate investors nationwide. With a focus on credit strategy and property-based underwriting, he helps clients optimize their approval odds, secure better loan terms, and grow their real estate portfolios with confidence.