DSCR Loans vs. Conventional Loans: Which is Better for Rental Properties?

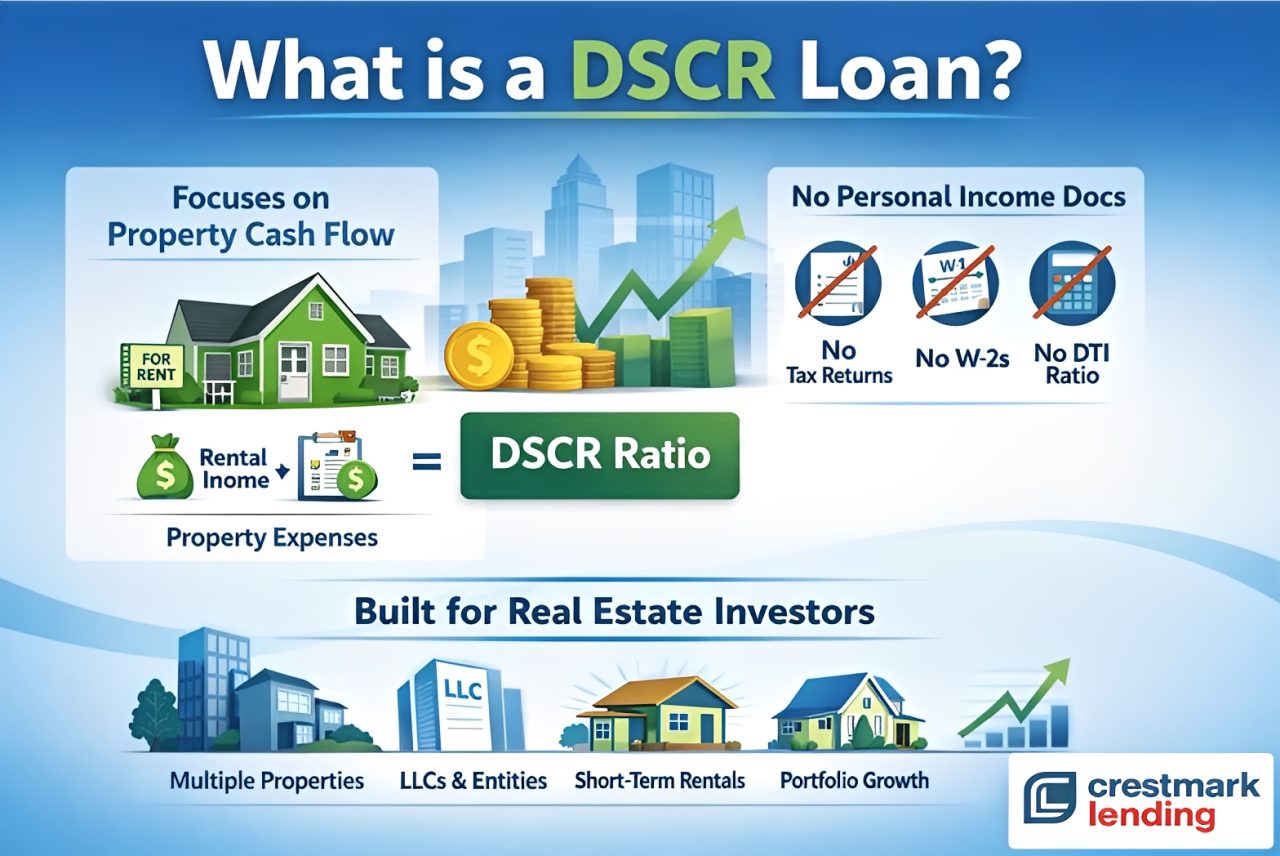

When it comes to financing rental properties, most investors eventually face the same question: Should I use a DSCR loan or a conventional loan? Both options can work—but they’re built for very different types of borrowers. Understanding the difference can help you choose the right strategy, qualify more easily, and scale your portfolio faster. What Is a DSCR Loan? A DSCR (Debt Service Coverage Ratio) loan is designed specifically for real estate investors. Instead of qualifying based on your personal income, lenders focus on the property’s cash flow. At Crestmark Lending, DSCR loans are built to help investors qualify using rental income—making them ideal for growing portfolios without traditional income limitations.- No W-2s or tax returns required

- Qualification based on rental income

- Ability to close in an LLC

- Designed for investment properties

- Based on income, employment, and credit

- Requires tax returns and W-2s

- Strict debt-to-income (DTI) limits

- Often limited to a certain number of properties

Key Differences: DSCR vs. Conventional Loans

Here’s where things really start to separate.- Income Qualification DSCR: Based on rental income Conventional: Based on personal income

- Documentation DSCR: Minimal (no tax returns required) Conventional: Full income documentation

- Property Limits DSCR: No set limit on number of properties Conventional: Typically capped around 10 financed properties

- Flexibility DSCR: Built for investors Conventional: Built for primary homebuyers

DSCR Loans = Built for Scaling • Conventional Loans = Built for Primary Buyers

DSCR vs. Conventional Loans

Here’s where things really start to separate.DSCR Loans

- ✔ Income Qualification: Based on rental income

- ✔ Documentation: Minimal (no tax returns required)

- ✔ Property Limits: No set limit on number of properties

- ✔ Flexibility: Built for real estate investors

Conventional Loans

-

- ✖ Income Qualification: Based on personal income

- ✖ Documentation: Full income documentation required

- ✖ Property Limits: Typically capped around 10 financed properties

- ✖ Flexibility: Built for primary homebuyers

When a DSCR Loan Makes More Sense

DSCR loans are often the better choice when your goal is to grow.- You already own multiple properties

- Your income is complex or self-employed

- You want to qualify based on cash flow—not tax returns

- You’re building a long-term rental portfolio

When a Conventional Loan Still Works

Conventional loans can still be useful in certain situations.- You’re buying a primary residence

- You have strong, stable W-2 income

- You’re early in your investing journey

- You want the lowest possible interest rate

Why Investors Transition to DSCR Loans

Most investors don’t start with DSCR loans—but many end up there. As portfolios grow, conventional financing becomes harder to use due to income limits and property caps. DSCR loans remove those barriers by focusing on what actually matters: Does the property cash flow? That shift makes it easier to continue acquiring properties without hitting traditional lending ceilings.Using the Crestmark DSCR Calculator

If you’re considering a DSCR loan, the first step is understanding your numbers. You can use the Crestmark Lending DSCR calculator to quickly determine:- If your deal meets DSCR requirements

- How much income your property needs

- Whether your investment will qualify

Final Thoughts: Choose the Loan That Fits Your Strategy

There’s no one-size-fits-all answer. Conventional loans can work well early on—but DSCR loans are built for scaling. If your goal is to grow a rental portfolio, simplify qualification, and focus on cash flow, DSCR financing is often the better long-term solution. And with the right lender, you can structure deals that support your growth—not limit it.This article was written by Ryan Collins of the Crestmark Lending team to help real estate investors understand the differences between DSCR and conventional loans. By choosing the right financing strategy, investors can qualify more easily, scale faster, and build stronger portfolios over time.