Thinking about financing a rental property or scaling your investment portfolio?

DSCR loans are a powerful tool that many investors are turning to — here’s why.

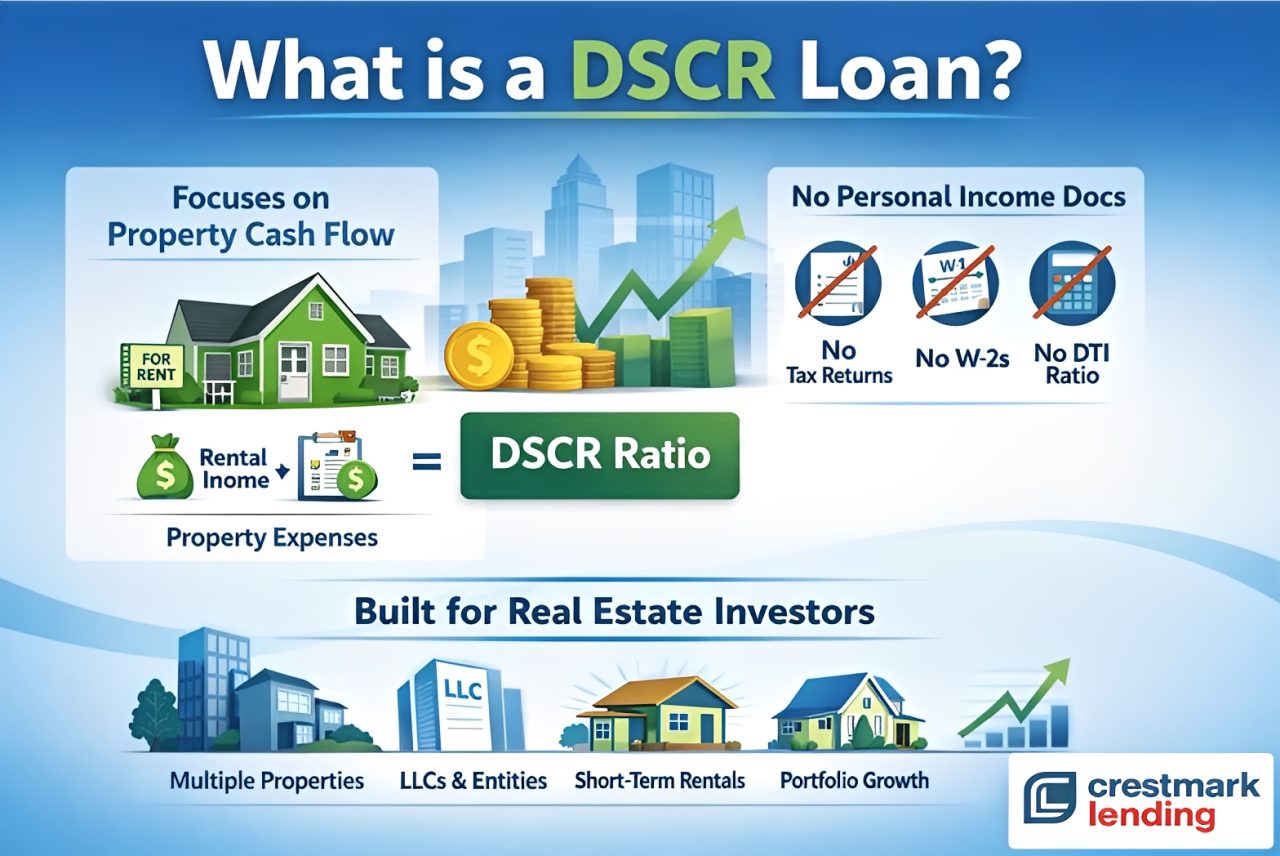

If you own rental property or are thinking about becoming a real estate investor, you’ve probably heard the term DSCR loan come up more and more over the last few years. But what exactly is a DSCR loan, and why are so many investors using them instead of traditional mortgages?

Let’s break it down in plain English.

What DSCR Means for Investors

DSCR stands for Debt Service Coverage Ratio.

In simple terms, it measures whether a rental property’s income is enough to cover its mortgage payment.

Instead of qualifying you based on:

- Personal income

- W-2s

- Tax returns

A DSCR loan looks primarily at the property’s cash flow.

If the rent covers the payment — or comes close — the property may qualify.

How a DSCR Loan Works

With a traditional mortgage, lenders focus heavily on your personal finances:

Tax returns

Debt-to-income ratio (DTI)

Employment history

DSCR loans flip that approach.

A DSCR lender evaluates:

Rental income from the property

Monthly mortgage payment (principal, interest, taxes, insurance, HOA)

The resulting DSCR ratio

Example:

If a property generates $2,500 per month in rent and the full mortgage payment is $2,200, the DSCR would be approximately 1.14.

Most DSCR lenders look for a ratio around 1.00 or higher, meaning the property can at least support itself. Use the DSCR Calculator to calculate your properties DSCR ratio.

| Item | Monthly Amount |

|---|---|

| Market Rent (or Lease Rent) | $2,500 |

| Total Monthly Housing Payment (PITI + HOA) | $2,200 |

| DSCR (Rent ÷ Payment) | 1.14 |

Why Investors Choose DSCR Loans

DSCR loans solve many limitations of traditional financing for real estate investors.

Here’s why they’re popular:

1. No Personal Income Qualification

DSCR loans do not rely on W-2 income, tax returns, or personal DTI. This is especially helpful for:

Self-employed investors

Business owners

Investors with aggressive write-offs

2. Ideal for Scaling Portfolios

Because the focus is on the property, not the borrower’s income, DSCR loans make it easier to:

Own multiple rental properties

Refinance properties without income bottlenecks

Continue growing without hitting DTI limits

3. LLC and Entity-Friendly

Most DSCR loans allow properties to be titled in an LLC or business entity, which many investors prefer for liability and accounting reasons.

4. Works for Many Property Types

DSCR loans can be used for:

Single-family rentals

Short-term rentals (Airbnb / VRBO, with lender approval)

2–4 unit properties

Small multifamily properties

Jumbo investment properties

DSCR Loan Benefits

- Qualify Using Rental Income

- Close in Your LLC or Business Entity

- Up to 80% LTV on Purchases & Refinances

- 30-Year Fixed and Interest-Only Options

- Eligible for Short-Term and Long-Term Rentals

- Fast Closings with Minimal Documentation

- No DSCR Seasoning Required

DSCR Ideal Borrowers

- Real estate investors

- Borrowers building a rental portfolio

- Airbnb & short-term rental hosts

- Self-employed investors

- BRRRR investors

- Buy-and-hold investors

Typical DSCR Loan Requirement

While guidelines vary by lender, most DSCR loans look at:

DSCR ratio: Often 1.00 or higher

Credit score: Commonly 660+

Down payment: Typically 20–25% for purchases

Reserves: A few months of payments in reserves

Property appraisal: Rent schedule or market rent

The exact terms depend on the lender, property type, and loan size. Learn more about DSCR Loan Requirements

| Requirement | Typical Guideline | Notes |

|---|---|---|

| Minimum Credit Score | 660+ | Some programs may allow lower with stronger overall file. |

| DSCR Ratio | ~1.00+ | Some lenders allow lower DSCR with higher down payment or reserves. |

| Down Payment (Purchase) | 20–25% | Varies by property type, loan size, and borrower profile. |

| Reserves | 3–12 months | Often higher for larger loans or multi-property portfolios. |

| Documentation | Light / property-focused | Typically no W-2s or tax returns required for qualification. |

| Eligible Properties | SFR, 2–4 units, some multifamily | Guidelines vary by lender and program. |

Are DSCR Loans Only for Experienced Investors?

No — both first-time and seasoned investors can use DSCR loans.

That said, DSCR loans are best suited for investors who:

Understand rental cash flow

Plan to hold properties long-term

Want flexible, scalable financing

If you’re buying your first rental or refinancing an existing property, a DSCR loan can still be a strong option.

DSCR Loans vs Conventional Investment Loans

Here’s the key difference:

Conventional loans qualify the borrower.

DSCR loans qualify the property.

Conventional loans can work well for small portfolios, but once investors scale, DSCR loans often become the more practical solution.

| Feature | DSCR Loan | Conventional Loan |

|---|---|---|

| Income Used | Property cash flow | Personal income |

| Tax Returns | Not required | Required |

| DTI | Not used | Required |

Is a DSCR Loan Right for You?

A DSCR loan may be a good fit if:

You want to avoid income documentation

Your properties cash flow or are close

You’re buying or refinancing investment property

You plan to scale a rental portfolio

The best way to know for sure is to review the property numbers with a lender who specializes in DSCR loans.

Final Thoughts

DSCR loans have become one of the most powerful financing tools for real estate investors. By focusing on property cash flow instead of personal income, they offer flexibility, scalability, and speed that traditional mortgages often can’t match.

At Crestmark Lending, DSCR lending isn’t a side product — it’s all we do. That focus allows us to help investors structure loans that actually support their long-term investment strategy.

This article was written by Ryan Collins of the Crestmark Lending team to help real estate investors better understand DSCR loans and how cash-flow-based financing works in real-world scenarios. The goal is to provide clear, practical insight so investors can make informed decisions when financing rental and investment properties.